Did you Know?

-Over 70% of Americans are financially stressed

-12% of Americans skip going to the doctor because of financial concerns

-80% of people admitted that their personal finances keep them awake at night

-21% of couples who rate their financial stress as at least “somewhat high” are arguing more

-32% of adults say their finances keep them from living a healthy lifestyle

You can combat these statistics! Here’s How:

7 Ways to START Taking Control of your Finances today

1. Cut Up all but 1 Credit Card

It’s a good idea to keep one credit card for those times that require a credit card to make reservations over the phone. Most things can be purchased with cash, paid by check or through your bank account with a bill pay service. I know many people that use credit cards to earn rewards and I’m not going to say you can’t do that if you are regularly tracking your expenditures and have a budget and pay that card off IN FULL every month.

However, it’s easy to overspend by using credit cards. If you truly are on a tight budget or just want to save everywhere possible and use that money for something else, using a cash system is going to really help you. It will cut back on impulse purchases and purchasing things you really don’t NEED.

2. Go on a Spending Freeze

What’s a spending freeze? It’s a specific period of time you basically freeze your finances. During this time period you won’t actively spend money, now you will however have to use money for things like utilities, groceries and supplies. You’ll want to stock up on necessities and get a meal plan for that time period you choose to get all the shopping done before the freeze. You can however, set some cash aside for fresh items like fruits, veggies, milk and bread you can’t totally pre-purchase.

It’s a great time to evaluate your spending priorities. What do you spend the most money on that’s not a necessary expense? Do you really find value in that expenditure?

Related Post: 5 Reasons to Do a Spending Freeze

3. Commit to Eating at Home

Buying your own groceries and cooking at home is plain and simply going to save you money. It’s also a healthier option. Yes, you’re going to need to plan and prepare, but you can do it! I have some meal planning tips you can read about to help you get started.

If you’re worried about missing out on social opportunities because of making meals at home, find other ways to connect socially. You could pack a lunch and meet someone at the park or go out to a movie instead. You can invite people to your house and cook them a meal. How about meeting a friend to walk or ride bikes?

4. Find a Mentor

Do you know someone that keeps their finances in order or has been able to wrangle them like a bull? IF you do, seek them out and ask them to help keep you accountable to the goals you are setting or ask them for help to set some goals. Perhaps you could meet with them once a month to track your progress or discuss anything that is causing you difficulty.

There are so many resources available for finances. Check out a book at the library or ask a friend to borrow one they have used.

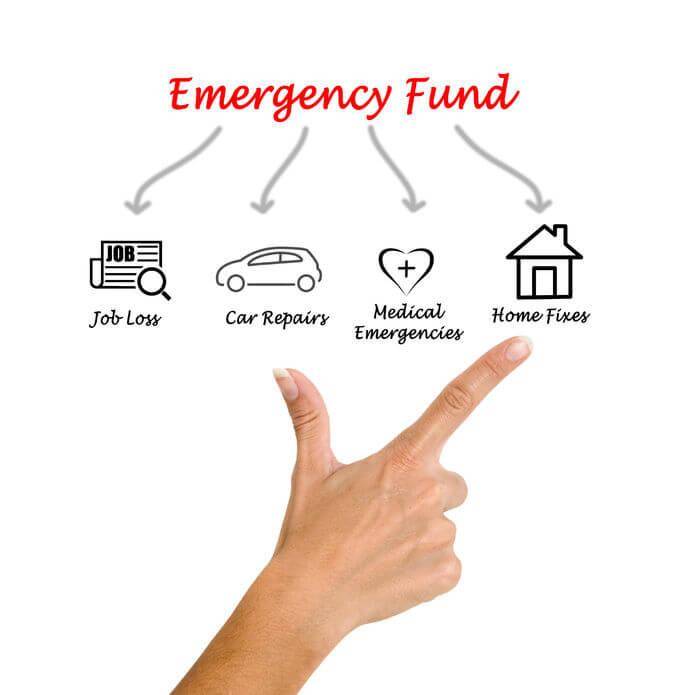

5. Build an Emergency Fund

You need a fund set aside for things that come up unexpectedly. If your car breaks down and you don’t have cash to pay for a large repair bill, you’re going to be more tempted to get a different vehicle (that ultimately costs more money) or put that expense on a credit card that you can’t pay off in the same month.

Just go to your bank and set up a savings account that’s specifically for emergencies. I have an automatic transfer set up from my checking to my savings account when I am scheduled to get paid so I don’t even think about having to do the transfer. (Honestly if I did I wouldn’t do it). Start small if you don’t have a large amount, but it will add up quickly. If you find that you have extra money you can ask your banker how to increase the automatic transfer. You can also just transfer money yourself, but don’t let yourself dig into that account unless it’s really for it’s intended purpose.

6. Set a Zero-Based Budget

Zero-Based budgeting is simply your income minus your outgoing expenses equaling zero. Now you aren’t spending all your money, but you are categorizing where each dollar goes including investments or savings so you end up with zero at the end of the month. I have some tips for creating a budget in my new book you can look into if you need help determinging how much should go into each category and what those categories should be.

7. Start Paying Down Debt

List your debts on a piece of paper. Pick the smallest debt first and pay it off. You still need to make minimum payments on your other debt, but your extra money can be used to pay off the smallest debt more quickly until it’s paid in full.

I’ve struggled with this concept called snowballing, but once I really thought it through I realized it really is a great way to get rid of your debt. Don’t start with your largest debt because you won’t feel the success of paying if off and it will be hard to keep going. If you pay off the smallest debt first you realize the freedom you feel and it will inspire you to tackle the next smallest debt!

Do you want to Take Control of Your Finances? Are you struggling to make a budget work, spending more than you’re making? This FREE 7 Day Financial Brilliance Challenge is for you! You’ll learn how to take control, get organized and make a budget work for you!